Written by Brian Frederick, CFP®, CIMA® & Trevor Marston

What We’re Seeing

“There’s no place like home.” – Dorothy

In honor of the release of the new cinematic version of Wicked, we thought we would take a moment to meditate on one aspect of L. Frank Baum’s classic story of The Wizard of Oz that seems particularly relevant to how most people view the financial markets today.

When it comes to the financial markets, it’s perfectly natural to feel a bit wary. After all, the markets often get portrayed as vast, intricate systems with seemingly endless streams of information and unpredictable outcomes. In many ways, they can feel like that first glimpse of the Wizard of Oz: a larger-than-life figure looming over everything, commanding attention and respect, yet shrouded behind curtains and special effects. There’s smoke, fire, and a booming voice behind a shimmering curtain. Fear, uncertainty, and the sense that someone else holds all the cards define the initial experience. To the uninitiated, it can feel overwhelming—like encountering a world that’s governed by forces too complex to fully grasp.

When Dorothy and her companions find the courage to look behind that curtain, they discover not a supernatural mastermind but a person simply using tools to project images and amplify sounds. The magic loses its mystique once the mechanism behind it is understood. Similarly, when we approach markets and finance from a different perspective, one of our goals, they lose much of their intimidation factor and become less of an unknowable force.

This clarity helps us focus on what we’re actually trying to achieve. Just as Dorothy’s true goal was to return home, our goals might be building a secure retirement, funding a child’s education, or leaving a charitable legacy. Staying grounded in our path allows us some intention and courage to look beyond the curtain of fearmongering headlines, the sensational 24/7 financial news cycle, and alarming predictions that tend to dominate attention. It allows us to realize we may have had the ruby slippers the entire time.

When we see the market as a tool rather than an imposing force, it becomes easier to filter out the noise by focusing on our goals and tried-and-true strategies: planning, controlling spending, and saving. Instead of being swayed by sensationalized predictions or fearmongering commentary, we remain grounded in a process that can help bring us all “home.”

5 Major Takeaways

- Inflation: Over the past quarter, but really going back to the beginning of 2024, headline inflation has shown a steady decline, reflecting easing supply chain pressures and an effective tightening cycle by the Federal Reserve. However, while the overall trajectory is downward, the Fed’s preferred inflation metric, Core PCE, has remained notably stable around 2.7-2.8%, underscoring the risk of inflationary surprises remains, particularly given geopolitical tensions and their impact on commodity markets, as well as a shift in US policy.

- Jobs: The U.S. labor market continues to display signs of resilience. With unemployment rates around 4%, the overall trend indicates a moderation in the labor market, though it is still far from a major contraction. This stability is supported by low layoffs and strong demand in key industries. Moving forward, the balance between wage pressures and economic growth is expected to influence the pace of further normalization. [Link]

- Chinese Stimulus: China’s economy shows signs of a bumpy recovery. Over the past 3 months, official data has reported strong GDP growth. However, steep declines in industrial profits underscore lingering structural challenges and weak demand. The Chinese government has rolled out significant stimulus measures, including interest rate cuts and a 6 trillion yuan ($839 billion) debt refinancing package for local governments. While the data suggests initial improvements, the effectiveness of these measures in driving sustained growth will depend on their ability to address deeper economic imbalances. [Link]

- Mortgage rates: As mortgage rates begin to decrease due to the Federal Reserve lowering interest rates, some homebuyers are feeling let down that the rates haven’t dropped more significantly. Currently, the average 30-year mortgage rate stands at 6.69% (as of 12/05), which is still relatively high, especially since 82.4% of existing mortgage holders enjoy rates lower than 5%. Additionally, 58% of homeowners in the U.S. have 30-year mortgages, and the low mortgage rates established during the pandemic continue to create a substantial wealth effect for these homeowners. [Link]

- Immigration: The Brookings Institute recently released a very comprehensive and somewhat technical overview looking at a variety of scenarios for immigration in a second Trump presidency. They take an even-handed view on why immigration is an increasingly important part of the US economy and what the fiscal and macroeconomic impacts of changes in immigration policy might look like. [Link]

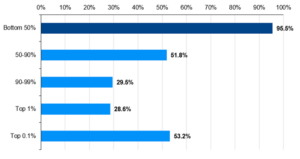

One Big Number

95.5%1

Since the pandemic, household net worth has surged, especially for the bottom 50%, but many households don’t feel this way. Consumer sentiment has been split starkly across political lines, which predictably reversed post-election. However, the truth is always somewhere in the middle. Consumers don’t often think about inflation levels or net worth; they think more about price levels, after-tax income, and spending on essentials as a percentage of their budget.

And One Big Chart

Percentage change in household net worth from 4Q 2019 to 2Q 2024 1

1 Source: Federal Reserve Distributional Financial Accounts, J.P. Morgan Asset Management. Data are as of October 25, 2024.

Opinions expressed in the attached article are those of the author/speaker and are not necessarily those of Raymond James. All opinions are as of this date and are subject to change without notice. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Including diversification as asset allocation. Past performance may not be indicative of future results. Prior to making an investment decision, please consult with your financial advisor about your individual situation. The stock indexes mentioned are unmanaged and cannot be invested into directly.