What We’re Seeing

“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.”

Sir John Templeton.

The narrative of financial markets in 2023 has been the tale of two markets to some degree. While the Federal Reserve continues driving the narrative, the real protagonist, so far, is Nvidia. With astronomical performance this year, combined with a few others such as Microsoft, and buoyed by the story of the transformative power of generative AI, these few heavyweights have carried the market virtually on their back. We should, however, never judge a book by its cover, and stories are never as simple as a headline.

How do we know the charge in equity markets has been led from only a narrow range of stocks? A statistic known as “market breadth” (a way of understanding the overall health of the stock market by looking at how many stocks are doing well versus doing poorly) is very narrow. Think of market breadth being narrow like watching a movie where the lead actors might be fantastic, but everyone else is just humdrum, the script is questionable, and the lighting isn’t great. The film might seem good for a little while, but if you watch it through to the end, it may not hold up.

While the key stars may dominate the narrative, we’ll look at a few other sub-plots at work and try to find some signal in the noise.

5 Major Takeaways

-

- AI!: With the power of generative AI now available for most to use, that story has dominated the headlines and the market movements. While we wait to see if it is the game-changer it is billed to be, we encourage you to have fun asking one of the many options out there to rewrite this article in the style of a famous literary figure such as Shakespeare, Jane Austen, or if you’re adventurous, William Burroughs.

-

- The Debt Ceiling: It came down to the wire, as it always does, but for the 79th time since 1960, Congress voted to raise the debt ceiling. The continued angst created around the debt ceiling can seem fraught in a contentious political environment. However, as we counseled clients, the stakes were high this time, and when it came down to it, cooler heads prevailed and there was a strong desire to get the deal done.

-

- The Housing Sector: A few critical economic data points, such as “Building Permits” and “Housing Starts,” have increased, indicating a rebound. The housing market remains resilient in the face of high interest rates. A key indicator that, if a recession were to occur, it could be mild.

-

- De-dollarization: The story of de-dollarization has been a talking point this past quarter, in some part due to the debt ceiling debate. As we wrote in a recent blog [Link], the topic is complicated, with no easy answers that can be summed up in a tidy headline or buzzword. This is not a short-term theme but something that would take years to play out and is far from certain.

-

- Stress in the Banking Sector: Though we’ve moved past the headline-grabbing failure of SVB, stress in the banking sector continues to weigh on liquidity and access to capital in the economy. The effects on lending can take 6 to 18 months to be felt in the economy. It’s a good reminder that the economy is not out of the woods yet, and a recession later in the year is possible.

One Big Number

$771 Billion1

The amount that Households still have left in excess pandemic-era savings. Since September 2021, that amount has been spent down by $1.4 trillion1. That extra spending added to inflation and dulled the impact of the Federal Reserve’s interest rate hikes. What impact does that have going forward?

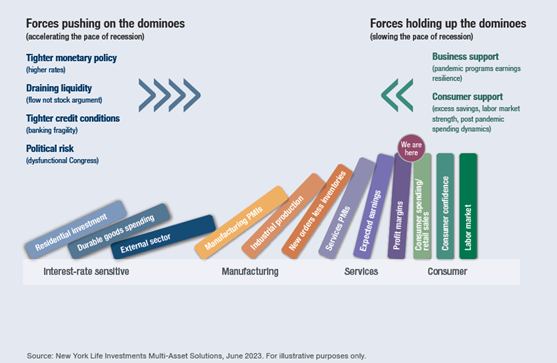

And One Big Chart

The strength of the financial landscape remains largely in the hands of the consumer. With $771 billion in excess savings remaining from the peak in May 2020, spending levels show resilience despite inflation and higher interest rates. In the labor market, workers are still scarce in key fields such as manufacturing and healthcare. Consumer confidence remains resolutely optimistic.

In conclusion, as we follow the story of 2023, let’s approach the financial markets with a healthy respect for plot twists. The bear market was with us for 17 months, but history shows us that the bad times don’t last as long as the good times. Earlier in June, the S&P 500 has risen more than 20% from the low reached in October 2022. A little early to call this a new bull market, but we have met the technical definition of one. So, let’s continue to turn the pages of this story together, embracing the challenges and opportunities that lie ahead, always moving forward.

1 Source: New York Life Investments Multi-Asset Solutions, U.S. Bureau of Economic Analysis, Macrobond, June 2023.

Any opinions are those of Brian Frederick and not necessarily those of Raymond James. This is not a recommendation to purchase or sell the stocks of the companies mentioned. Expressions of opinion are as of this date and are subject to change without notice. Past performance may not be indicative of future results. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.