What We’re Seeing

“Know what you own, and know why you own it” – Peter Lynch

At the beginning of 2023, the prevalent view was a looming recession. Yet, The S&P500 surprised many by delivering a 26.18% total return. Even the Bloomberg Aggregate US Bond index clawed its way back from another choppy year to a 5.65% total return. Not too bad. Even more surprising, much of that came in the last six to nine weeks of the year. Janet Yellen even mentioned that we have officially landed softly [Link]. That’s what we call a “rebound.”

Of course, that came on the heels of one of the harder years in 2022 when the S&P 500 and bonds were down. At the beginning of that year, many could foresee that it would be a tough year with soaring inflation, but many also thought that the rocket ship performance of 2021 may continue unabated. It’s hard to know.

What if our job isn’t to know? What will we do in the face of uncertainty (and when can we think of a time more uncertain than how much of the world seems right now)? Maybe the answer is to focus on real-world goals, turning “what-ifs” into “what-nows.” Instead of comparing ourselves to some ideal (a stock index), it’s often better to keep our eyes on how we can meet our obligations, attain our goals, and the possibilities we might not have if something were to happen.

This is a complex problem; it may be even more complex than predicting what the market does from a certain perspective. It’s certainly a more impactful problem, and it brings to bear a number of tried-and-true concepts we continually preach. Playing defense, thinking broadly about diversification, staying the course, tuning out the noise, and knowing where you’re going. Armed with those first principles, we can still find a signal through the noise even when people are keen with despair or clamor with elation. Here’s to an uncertain 2024.

5 Major Takeaways

- Elections: As we approach another contentious election, it’s pertinent to look back and consider its possible impact on investment performance. It can create ups and downs, but those are largely short-term, and economic and inflation trends matter more. U.S. Bank wealth management has an excellent article [Link] that performs a statistical analysis of a number of historical scenarios and finds that only a few election outcomes are even statistically significant.

- A Divided Economy: While much of the 2023 economic data from the Federal Reserve pointed to a contracting domestic manufacturing sector, the services sector continued stubbornly expanding. However, with more recent data showing some softening in the services sector as well and interest rates potentially set to decline, the manufacturing sector may find it has some runway ahead.

- Credit: While most corporations and households took advantage of lower rates during COVID, a raft of corporate debt maturities beginning in 2025 will likely stress credit markets. However, it remains to be seen whether this risk will rise to the level of concern. If you want to dive deeper, Axios Markets has more [Link]

- ESG: In October, the IMF published a thorough analysis [Link] of some of the fiscal policies around the world in the “global coordination to push forward pragmatic climate goals.” Low-carbon and renewable technologies continue to see concentrated policy support around the globe as governments and corporations alike have taken a firmer hand in managing climate risks. The issue also dives straight to the heart of energy independence and is set to continue to have a strong tailwind.

- Housing: One stubborn contributor to inflation and the strength of the US economy in the face of rising interest rates has been strength in the housing market. There aren’t many houses for sale right now, as existing home sales in October dropped to their lowest level in 13 years, with an additional dip in November. However, initiatives like the one in NYC [Link] to convert some vacant office space into residential housing are gaining strength.

One Big Number

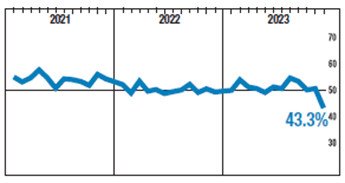

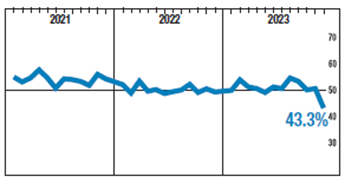

43.3%1

December 2023’s ISM Services Employment index. [Link]. The ISM indicators are somewhat confusing statistics, but simply if the number is above 50, the sector is expanding, and if it’s below 50, it’s contracting. In the case of our ISM Services Employment indicator, this number is contracting and is off a sharp 7.4% from the previous indicator.

And One Big Chart

1

1

This is a chart of the ISM Services Employment index over the last three years. Until now, the services sector has been the strongest and most stubborn part of the US economy in the face of rising interest rates and inflation. However, the notable cooling near the end of the year indicates there may have been a sharp turn in that narrative. Suggesting a more muted 2024 might be in store for the services sector as a whole.