Brian Frederick, CFP®, CIMA®

We are all hearing a lot of commentary about the spread of the coronavirus. It is concerning because no one knows for sure how fast and far it will spread and what sort of lethality it carries. The first US case of the coronavirus was in Snohomish County and after a quarantine he was released and is back at work now. Let’s hope that 99.9% or more of the cases are like that. That would make it the same as the common flu in the United States. People are fearing that it will be much worse and that it will have a lasting impact on the world’s economy. The next month or two will help determine what the health and economic ramifications are, but what are investors to do in the meantime?

While we all know that markets don’t go up every day or move in a straight line, it is never fun to watch the market gyrate. During these times it is difficult to stay with the investment plan, but it is important to stick with it.

Investment psychology plays an important role for successful, long term investors. One of the main reasons or biases that people have is called loss aversion. Essentially, the average person experiences twice the amount of pain from a 10% drop in investments as they feel joy in a similar 10% gain. Loss aversion creates stress and during these emotional times, people do what feels good and sell. This stops the pain temporarily, but it is proven that getting back in at the right moment is almost impossible. This bias is the main force behind the growing field of behavioral finance.

It is also one of the things that we count on in our investment strategy. We know markets react and go to extremes at times. This can be measured many different ways, but our process employs rebalancing. All rebalancing does is systematize selling high and buying low. Our last rebalance was done on 12/23/19. We did it to lock in some of the profits from a great year and reduce the risk in preparation for the expected ups and downs of the market in an election year.

We are nearing another point of rebalancing to take advantage of the dislocation in the market.

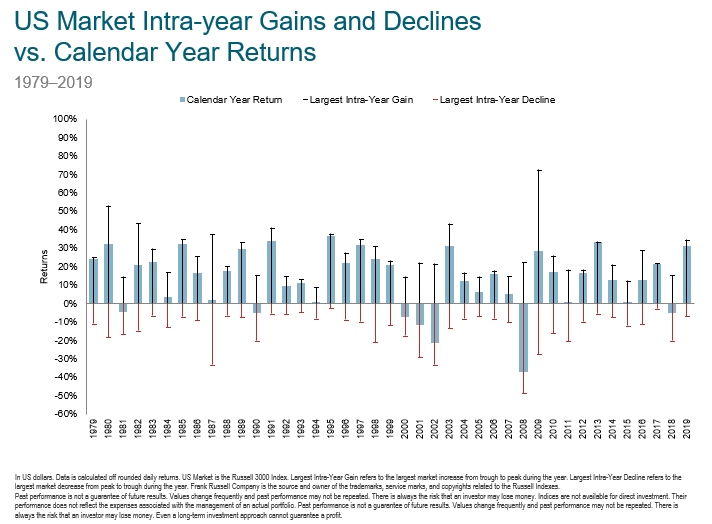

The chart below shows the last 40 years of market returns by year and also the fluctuations from the highest point to the lowest. Every year there have been fluctuations and most have seen pretty dramatic movements. Rebalancing helps us take advantage of these opportunities.

Source: Dimensional Advisors Fund LP Presentation

The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete nor is it a recommendation. Any opinions are those of Brian Frederick are not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor’s results will vary. Past performance does not guarantee future results. Future investment performance cannot be guaranteed, investment yields will fluctuate with market conditions.

Rebalancing a non-retirement account could be a taxable event that may increase your tax liability.

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

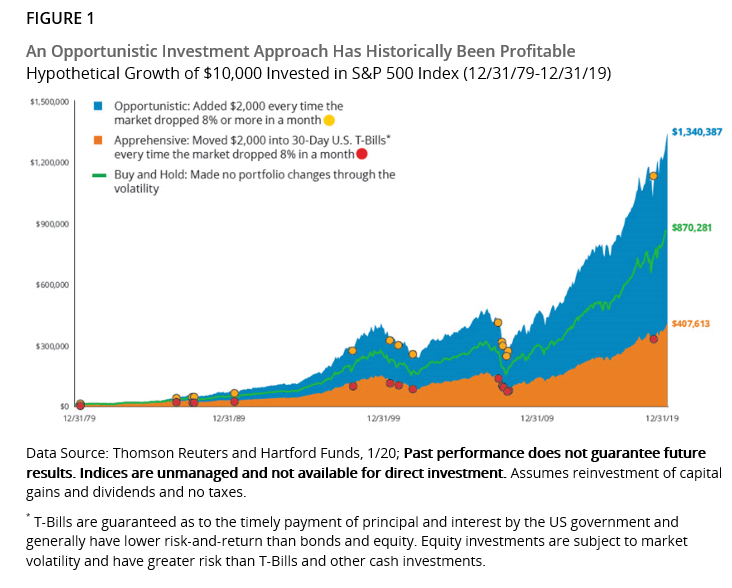

Figure 1 is a hypothetical illustration and is not intended to reflect the actual performance of any particular security. Future performance cannot be guaranteed, and investment yields will fluctuate with market conditions.

Certified Financial Planner Board of Standards Inc. (CFP Board) owns the certification marks CFP®, Certified Financial Planner™, CFP® (with plaque design), and CFP® (with flame design) in the U.S., which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.